Two kinds of fraud hit small and mid-size businesses hard — and they share a root weakness: a legitimate-looking channel nobody double-checks.

| Side | Failure mode | Downstream damage |

|---|---|---|

| Your domain | Soft SPF / DMARC / MTA-STS lets criminals impersonate @yourfirm.com | Wire fraud, fake invoices, password-reset traps aimed at clients and vendors |

| Everyday payments | Typing or swiping the real card at every checkout / pump / convenience ATM | Skimming, Magecart form theft, and card fraud that’s hard to trace |

This guide covers both: what 100% actually means on an EmailMeNow domain audit, and the habits — tokenized checkout, Tap to Pay, virtual card numbers, skimmer checks, alerts, MFA — that keep your business and your customers’ cards safer.

Domain scores below come only from audit.emailmenow.com. CMS / stack notes come only from our website-tech probes — not Mozilla Observatory, SSL Labs letter grades, or invented “98%” tables.

What a 100% Domain Security Score Requires

At EmailMeNow, 100% is the ideal — full coverage across the layers criminals actually abuse — not a “good enough” grade with one checkbox left open. A free scan at audit.emailmenow.com evaluates:

| Layer | What’s checked | Why it matters |

|---|---|---|

| Email authentication (Identity) | SPF, DKIM, DMARC — ideally p=reject | Stops mail that only looks like it came from your domain |

| Transport security | MTA-STS (ideally enforce) and TLS-RPT style reporting | Stops silent downgrade of inbound mail to weaker encryption |

| Website security | HSTS, CSP, frame controls, related headers | Reduces clickjacking / script-injection exposure on public pages |

| Hardening signals | Infrastructure and endpoint-related posture in the report | Shrinks what attackers can casually probe |

Domains rarely fail every layer. More often one gap caps the whole score — classic pattern: SPF present, DMARC still monitoring (or soft), no MTA-STS. That profile shows up across industries; for one published sample see Top Nevada law firms email security audit (2026).

Business takeaway: a domain stuck in the midrange is the one criminals spoof for BEC / invoice fraud. Harden your mail before you coach customers on card hygiene — run audit.emailmenow.com on your primary domain, then contact us if you need help closing gaps (College Station, Texas; law firms, healthcare, CPAs, dealers, title, advisors, schools, and local government).

Quick Decision Guide (cards)

| Situation | Safer default | Why |

|---|---|---|

| Online checkout | Wallet / Stripe Link / PayPal / Click to Pay or a virtual card number | Merchant never stores (or rarely sees) your real PAN |

| In-store reader | Tap to Pay (phone, watch, or contactless card) | Terminal gets a token / dynamic cryptogram, not your durable card number |

| Gas pump / unattended kiosk | Pay inside, or tap with a wallet; use credit not debit | Outdoor pumps and freestanding ATMs are skimmer favorites (FBI) |

| Cash from ATM | Bank-branch or cardless ATM via your bank app | Convenience-store ATMs are frequent overlay targets |

| Recurring SaaS / store account | Link a virtual or tokenized method once | Limits blast radius if that one merchant is breached |

Stop Entering the Real Card on Every Site

Every time you type PAN + expiry + CVV into a standard HTML form, you expose that data to several vectors:

| Vector | What happens |

|---|---|

| Keyloggers | Malware on your device records keystrokes before encryption helps |

| Magecart / digital skimming | Malicious JavaScript on a merchant checkout page intercepts the form as you type |

| Merchant database breaches | Stored PANs leak months later in breach dumps |

| Support / phishing pages | Fake “update your billing” forms that look like the real brand |

Prefer tokenization and digital wallets

Instead of sharing your Primary Account Number (PAN) with every shop:

| Option | What you gain |

|---|---|

| Google Wallet / Apple Pay / Samsung Pay | Device unlock + network token / Device Account Number; often useless if stolen out of context |

| Stripe Link | Returning checkout on participating sites without retyping the full PAN |

| PayPal | Layer between merchant and funding source when Link / Wallet isn’t offered |

| Click to Pay (card-network option) | Network-level recognition so you aren’t pasting the embossed number on every site that supports it |

Tokenization means the merchant and many middle hops see a stand-in. Your embossed plastic number stays with the wallet issuer or bank.

| Habit | Do this |

|---|---|

| First visit to a store | Prefer Wallet / PayPal / Link / Click to Pay when offered |

| Guest checkout | Prefer one-time or merchant-locked virtual numbers from your issuer |

| “Save card for later” | Only on merchants you trust — still prefer a wallet token or virtual PAN |

| Business travel sites | Use a virtual number with a spend or expiration limit |

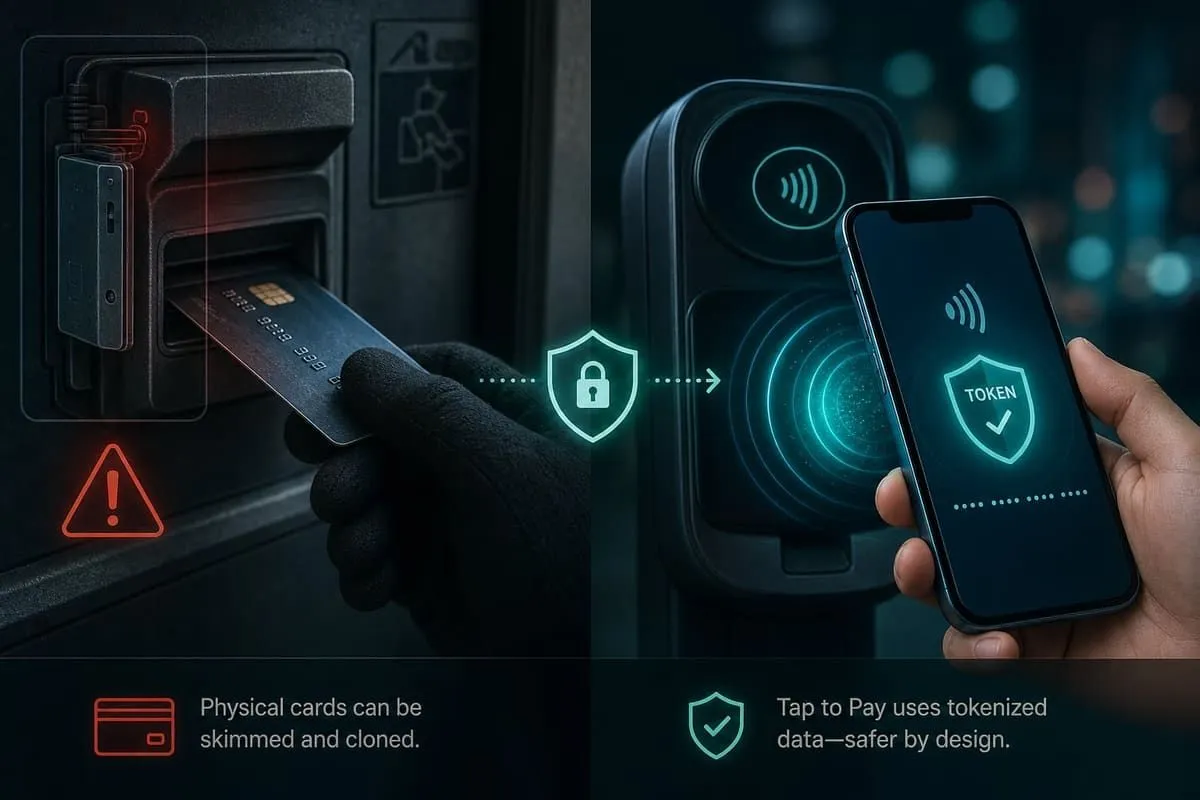

Eradicate Unnecessary Physical Card Contact

Tap to Pay, watches, and linked store cards

| Method | Why it beats a swipe / insert |

|---|---|

| Phone or watch Tap to Pay | PAN is not exposed the same way a magstripe swipe is |

| Contactless chip card tap | Better than swipe; phone wallets stay stronger if the plastic is later cloned |

| Store / membership linked to a CC | Example pattern: warehouse-club cards (e.g. Costco Anywhere Visa by Citi) linked in the merchant app so membership + pay can run from the account/app barcode without handing over plastic every visit |

Physical plastic is a backup — not the daily driver for pumps, corner stores, and random e-commerce.

Skimmers, Shimmers, and Freestanding ATMs

The FBI describes illegal devices on ATMs, POS terminals, and fuel pumps — including overlays and gear on exposed cables at freestanding convenience-store ATMs. The U.S. Secret Service leads many access-device fraud cases at pharmacies, grocery stores, and gas stations.

2025 scale (official): In a January 2026 release, the Secret Service reported 22 EBT/ATM skimming outreach operations, 411 illegal devices removed, nearly 60,000 terminals inspected, and an estimated $428.1 million in potential loss prevented. Early 2026 city operations continued that pattern (dozens more devices pulled in cities such as Cleveland and Denver).

Local example (July 2026): The Caroline County (VA) Sheriff’s Office warned after a skimmer was found on a gas-station ATM near I-95 (Pit Stop Exxon, Ladysmith). Officials described a near-exact replica overlay of the ATM’s top portion; reporting noted these overlays are often Bluetooth-equipped so thieves can download stolen card data without removing the device. Travelers using interstate convenience ATMs should treat that as a standing risk pattern — not a one-off Virginia quirk.

Industry analysts still flag non-bank / standalone ATMs as a disproportionate compromise location versus branch machines (ABA summary of FICO Card Alert trends — bank ATMs were still roughly a quarter of compromise locations in that reporting, not “safe by default”).

| Device type | Rough idea |

|---|---|

| Skimmer | Overlay or internal capture aimed at magstripe / reader data (some store data for Bluetooth pickup) |

| Shimmer | Thin insert inside a chip slot meant to intercept EMV traffic |

| Hidden camera / keypad overlay | Captures PIN while the reader steals card data |

| POS overlay | Seconds-long install; FBI notes distraction of clerks (e.g. asking for an item behind the counter) while a device is placed |

Five-second reader check (wiggle test)

| Check | What to look for |

|---|---|

| Wiggle / tug | Gently pull the card bezel — legitimate slots feel solid; overlays often shift |

| Fit / color | Bulky, crooked, mismatched graphics vs. neighboring pumps |

| Residue | Glue, tape, scratches, broken security seals |

| Keypad | Spongy overlay; cover the PIN with your hand anyway |

| Location | Prefer pumps near the attendant; indoor, well-lit, bank-attached ATMs |

| Outcome | If the ATM keeps your card, call the issuer immediately |

Capital One’s consumer guidance stresses contactless payments, digital wallets, and cardless ATM withdrawals where supported.

How to avoid dipping a card at a risky ATM

| Prefer | Avoid when you can |

|---|---|

| Cash from a bank-branch ATM or teller | White-label ATM inside a convenience store |

| Cardless ATM in your bank app (Chase Cardless Cash, Bank of America Cardless Cash, and similar features at other banks) | Swiping magstripe “for older machines” |

| Credit (issuer floats the risk) if you must dip | Debit + PIN at an unattended pump |

| Pay for fuel inside; or run debit as credit to skip the PIN when the terminal allows | Outer-island pumps that feel “upgraded” with odd bezels |

Virtual Credit Cards — One Number Per Merchant

Virtual account numbers (VANs) let Capital One, Citi, and others issue a unique card number tied to your real line of credit — often merchant-locked or limited by date / amount.

[ Your real credit account ]

│

┌────────┴────────┐

▼ ▼

[ Merchant A VCC ] [ Merchant B VCC ]

only works at A only works at B| Issuer pattern | Practical use |

|---|---|

| Capital One virtual card numbers (Eno / app) | Store-specific or general virtual numbers; lock or delete after suspicious activity (overview) |

| Citi virtual account numbers | Generate before checkout; set expiration / limits when available |

| Privacy.com / bank equivalents | Useful when your primary issuer lacks clean virtual numbers |

Rule of thumb: one virtual number per recurring merchant (streaming, SaaS, that one sketchy shop). If the merchant is breached, you kill one token — not every autopay in your life.

Harden the Account Perimeter

| Control | Why it matters |

|---|---|

| Push alerts at $0.01 (or the lowest threshold) | Spot micro-authorization tests before a big fraud wave |

| MFA — prefer authenticator app or passkeys / hardware keys over SMS | SIM-swap still breaks SMS OTP on bank and wallet portals |

| Card Lock in the issuer app | Keep seldom-used plastics locked until the moment of purchase |

| Prefer credit over debit for day-to-day spend | Debit + PIN is skimmer gold against your checking balance |

| Password manager + unique passwords | Bank credential reuse turns one breach into account takeover |

| Credit freeze / lock when not applying | Blocks new accounts opened with stolen identity data |

| Don’t text photos of your card | Support scams still harvest PAN + CVV from “verify” requests |

| Shred retired plastics | Embossed numbers still fuel card-not-present testing |

| Review recurring charges monthly | Replace stored PANs with virtual numbers where possible |

| Business cards on a separate account | Softens blast radius for company SaaS vs. household spend |

| Phishing-resistant habit | Never follow “fraud team” links in unexpected mail/SMS — open the official app |

| Smishing after a skim | Stolen cards are often followed by texts impersonating the bank’s fraud desk to harvest CVV or OTP — a real bank won’t ask for those over text |

| Fast dispute | Most issuers zero-liability unauthorized charges reported promptly |

| Guest checkout on one-off merchants | Nothing durable sitting in that merchant’s vault for the next breach |

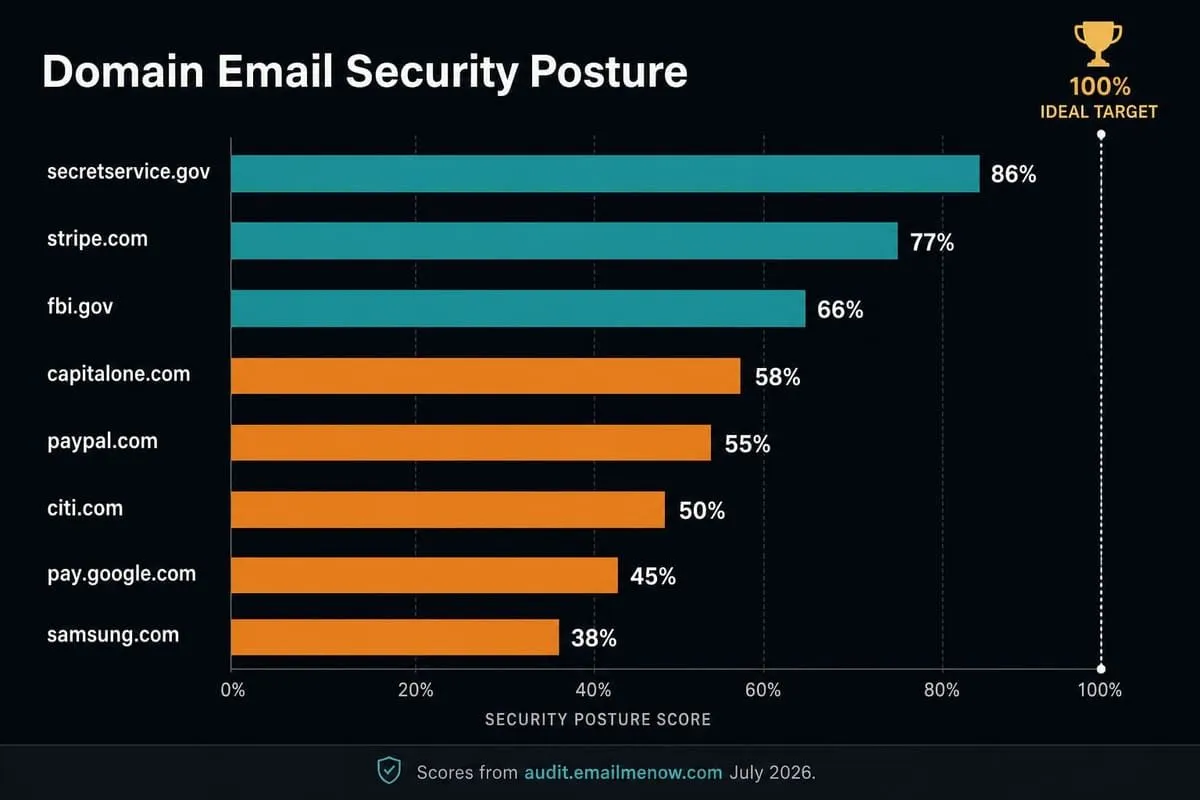

Payment & Authority Domains We Scored

Authority for these scores: audit.emailmenow.com only (EmailMeNow identity, transport, and website scoring). 100% is the ideal. Snapshot date: July 14, 2026. Sorted highest → lowest.

| Domain | Overall | Identity | Transport | Website | Level |

|---|---|---|---|---|---|

| secretservice.gov | 86% | 90% | 45% | 92% | Strong |

| stripe.com | 77% | 65% | 15% | 100% | Good |

| fbi.gov | 66% | 75% | 45% | 45% | Above Average |

| capitalone.com | 58% | 60% | 15% | 45% | Average |

| paypal.com | 55% | 60% | 45% | 45% | Average |

| citi.com | 50% | 40% | 15% | 45% | Average |

| pay.google.com | 45% | 0% | 15% | 92% | Below Average |

| samsung.com | 38% | 10% | 15% | 45% | Weak |

| Finding | Detail |

|---|---|

| Ideal score | 0 of 8 at 100% overall |

| Soft transport | Several payment brands at 15% Transport — limited encrypted-mail transport posture on the scored hosts |

| Soft identity | Weak Identity on pay.google.com / samsung.com → spoofed “wallet security” mail risk |

| Strongest here | secretservice.gov (86%); Stripe Website category at 100% |

| Consumer takeaway | Use their payment products; still open the official app for security events — don’t trust inbound email alone |

Third-party header letter grades (Mozilla Observatory, SSL Labs A/B scales, invented 90–98% tables) are not used here and are not interchangeable with EmailMeNow overall scores.

Run or refresh any score yourself: stripe.com · paypal.com · pay.google.com · capitalone.com · citi.com · samsung.com · fbi.gov · secretservice.gov

Website stack note (website-tech authority)

Passive website-tech probes on July 14, 2026 covered all eight domains (8 probed, 1 notable):

| Domain | Notable finding |

|---|---|

| secretservice.gov | Drupal reports major 11 while latest patch line is 11.4.3 |

| Others | No notable outdated CMS / PHP / short-horizon TLS alerts in this pass |

Stack freshness is a separate signal from card tokenization quality. For readers, the win is still how you present the card, not chasing a government site’s Drupal minor version.

15-Minute Setup Checklist

| Step | Action |

|---|---|

| 1 | Scan your business domain at audit.emailmenow.com — aim for 100% (DMARC reject + MTA-STS) |

| 2 | Install Google Wallet (or Apple Pay) and add your primary credit card |

| 3 | Set issuer push alerts to the lowest amount (ideally every charge) |

| 4 | Enable app / passkey MFA on bank, card, PayPal, and email (avoid SMS-only) |

| 5 | Create a virtual number for your next new subscription |

| 6 | Find cardless ATM in your bank app; practice once at a branch machine |

| 7 | Default online checkout to Link / PayPal / Wallet / Click to Pay, not manual PAN entry |

| 8 | Lock seldom-used plastics in the issuer app |

The Common Thread

A spoofed domain and a skimmed card both exploit trust in a channel that looks normal. DMARC p=reject + MTA-STS closes the email gap for your firm. Tokens, Tap to Pay, virtual numbers, and a five-second tug on the reader close it for payments. Neither takes long — both are cheaper than the fraud they prevent.

Run a free domain scan: audit.emailmenow.com

Need help closing gaps? Contact EmailMeNow — College Station, Texas.

Related Resources

- FBI — Skimming

- U.S. Secret Service — ATM & POS skimming

- Secret Service — 2025 skimming outreach results

- WRIC — Caroline County VA ATM skimmer warning (July 2026)

- Capital One — Credit card skimmers

- Capital One — Virtual card numbers

- Forbes Advisor — credit card processing overview (merchant side)

- Top Nevada law firms email security audit

- Texas real estate wire fraud / BEC

- Gmail calendar phishing protection

Educational overview for EmailMeNow readers (College Station, Texas and remote). Not legal, tax, or bank advice. Card terms and virtual-number features vary by issuer and product; confirm in your bank’s app. Domain scores: audit.emailmenow.com only. Stack notes: website-tech probes only. Snapshot July 14, 2026.